Very Short Answer Type Questions

Question. Define marginal product.

Answer : Marginal product is net addition to total product when one additional unit of variable factor is used.

Question. Why does the difference between average total cost and average variable cost falls with increase in output?

Answer : It is because average fixed cost goes on falling with increase in output.

Question. At what rate average and marginal revenue falls, with fall in per unit price of a good?

Answer : Marginal revenue falls twice the rate of average revenue.

Question. What do you mean by marginal revenue?

Answer : Marginal revenue is net additions to total revenue by sale of one additional unit of output.

Question. Why does average cost curve and averages variable cost curve never intersect each other?

Answer : Because AFC can never be zero at any level of output.

Question. State any two conditions of producers equilibrium according to marginal revenue and marginal cost approach.

Answer : 1. MR = MC

2. Rising portion of Marginal cost curve intersects marginal revenue curve.

Question. What do you mean by individual supply schedule?

Answer : Individual supply schedule is a tabular representation showing various quantities of a commodity which a firm is ready to sell at different prices during a given period of time.

Question. Name two determinants of supply.

Answer : 1. Number of firms

2. Change in technology

Question. What type of change in price is the cause of upward movement along a supply curve?

Answer : Due to increase in price.

Question. What causes a downward movement along a supply curve?

Answer : Decrease in price.

Question. How does a decrease in price of input effect supply curve of the commodity?

Answer : As a result of decrease in price of input production cost falls then producers profit margin will increase so producer will increase the supply of commodity.

Question. What is meant by elasticity of supply?

Answer : Price Elasticity of Supply (Es) is a measure of degree of response of supply for a good to change in its price.

Question. When does the elasticity of supply of commodity called equal to unity?

Answer : When percentage change in price is equal to percentage change in supply.

Question. What causes an extension in supply?

Answer : Increase in price of a commodity.

Short Answer Type Questions

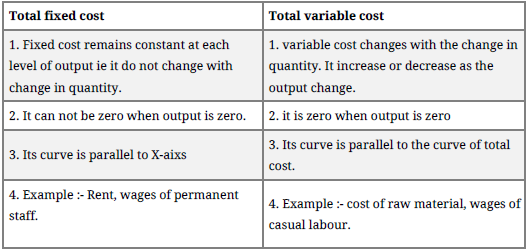

Question. With the help of example distinguish between total fixed cost and total variable cost.

Answer :

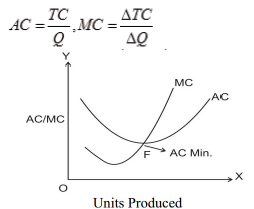

Question. Draw average cost, average variable cost and average fixed cost curves on a single diagram and explain their relation.

Answer :

1. AC is the vertical summation of AVC and AFC

2. The difference between AC and AVC falls as output increases but the difference of AC and AFC increases.

3. As output increases AC and AVC tends to be closer but theircurves do not interect each other because AFC always remains more than zero.

Question. Explain the relationship between AC & MC with diagram.

Answer :

(i) When MC < AC, AC falls.

(ii) When MC = AC, AC is minimum.

(iii) When MC > AC, AC rises.

(iv) MC falls & rises faster than AC.

(v) Both are obtained from TC.

Question. How do changes in MR affect TR?

Answer :

1. If MR increases, TR increases at increasing rate.

2. If MR is constant, TR increases at constant rate.

3. If MR falls, TR increases at diminishing rate.

Question. What will be the price elasticity of supply if the supply curve is a positively sloped straight line?

Answer : Es = 1 if the curve starts from the origin point.

Es>1 if the curve starts from the y-axis and

E<1 if the curve starts from the x-axis.

Question. Explain how do the following determine price elasticity of supply:

(i) Nature of the good

(ii) Time period.

Answer :

1. Nature of Commodity – Elasticity of industrial goods is more than that of agricultural goods. Similarly supply of durable goods e.g. table is more elastic than that of perishable goods e.g. vegetables.

2. Time Period- Generally elasticity of supply is more in the long period than in shorter period of time. The reason is that in the long period, all adjustments to the changed price can be made easily and supply of commodity can be varied accordingly.

Long Answer Type Questions

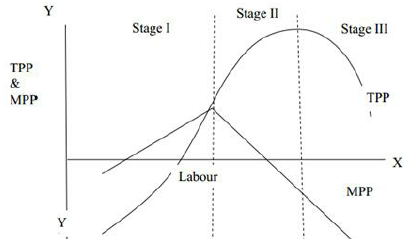

1. In the following table, identify the different phases of the law of variable proportions and explain them with the help of the table and a diagram.

Ans. Law of Variable Proportion states that if we go on using more and more units of a variable factor along with a fixed factor, the total output initially increases at an increasing rate, after that it increases at diminishing rate and finally it declines.

It can be explained through the following three stages:

Stage 1:

• TPP increases at an increasing rate.

• MP increases and reaches at its maximum at the end of the stage.

• This is also called stage of increasing returns.

Stage 2:

• TPP increase but at diminishing rate.

• MPP starts decline but remains positive.

• This stage comes to an end when TPP is maximum and MPP is zero.

Stage 3:

• TP starts decline.

• MP becomes negative.

• This is also called stage of decreasing/negative returns.