Please refer to Class 12 Accountancy Sample Paper Term 1 Set A with solutions below. The following CBSE Sample Paper for Class 12 Accountancy has been prepared as per the latest pattern and examination guidelines issued by CBSE. By practicing the Accountancy Sample Paper for Class 12 students will be able to improve their understanding of the subject and get more marks.

CBSE Class 12 Accountancy Sample Paper for Term 1

Part – I

Section – A

1. Gain/loss on revaluation at the time of change in profit sharing ratio of existing partners is shared by (i) ……… whereas in case of admission of a partner it is shared by (ii) ……… .

(a) (i) remaining partners, (ii) all partners

(b) (i) all partners, (ii) old partners

(c) (i) new partner, (ii) all partner

(d) (i) sacrificing partner, (ii) incoming partner

Answer

B

2. Calculate the amount of second and final call when Abhijit Ltd, issues equity shares of ₹ 10 each at a premium of 40% payable on application ₹ 3, on allotment ₹ 5, on first call ₹ 2.

(a) Second and final call ₹ 3

(b) Second and final call ₹ 4

(c) Second and final call ₹ 1

(d) Second and final call ₹ 14

Answer

B

3. Anish Ltd, issued a prospectus inviting applications for 2,000 shares. Applications were received for 3,000 shares and pro-rata allotment was made to the applicants of 2,400 shares. If Dhruv has been allotted 40 shares, how many shares he must have applied for?

(a) 40

(b) 44

(c) 48

(d) 52

Answer

C

4. Ambrish Ltd offered 2,00,000 equity shares of ₹ 10 each, of these 1,98,000 shares were subscribed. The amount was payable as ₹ 3 on application, ₹ 4 on allotment and balance on first call. If a shareholder holding 3,000 shares has defaulted on first call, what is the amount of money received on first call?

(a) ₹ 9,000

(b) ₹ 5,85,000

(c) ₹ 5,91,000

(d) ₹ 6,09,000

Answer

B

5. What will be the correct sequence of events?

(i) Forfeiture of shares

(ii) Default on calls

(iii) Reissue of shares

(iv) Amount transferred to capital reserve Codes

(a) (i), (iv), (ii), (iii)

(b) (ii), (iv), (i), (iii)

(c) (ii), (i), (iii), (iv)

(d) (iii), (iv), (i) (ii)

Answer

C

6. Arun and Vijay are partners in a firm sharing profits and losses in the ratio of 5:1.

If the value of machinery reflected in the balance sheet is overvalued by 33 %, find out the value of machinery to be shown in the new balance sheet.

(a) ₹ 44,000

(b) ₹ 48,000

(c) ₹ 32,000

(d) ₹ 30,000

Answer

D

7. Which of the following is true regarding salary to a partner when the firm maintains fluctuating capital accounts?

(a) Debit Partner’s Loan A/c and Credit P & L Appropriation A/c

(b) Debit P & L A/c and Credit Partner’s Capital A/c

(c) Debit P & L Appropriation A/c and Credit Partner’s Current A/c

(d) Debit P & L Appropriation A/c and Credit Partner’s Capital A/c

Answer

D

8. At the time of reconstitution of a partnership firm, recording of an unrecorded liability will lead to

(a) gain to the existing partners

(b) loss to the existing partners

(c) Neither gain nor loss to the existing partners

(d) None of the above

Answer

B

9. E, F and G are partners sharing profits in the ratio of 3 : 3 : 2. According to the partnership agreement, G is to get a minimum amount of ₹ 80,000 as his share of profits every year and any deficiency on this account is to be personally borne by E. The net profit for the year ended 31st March, 2021 amounted to ₹ 3,12,000. Calculate the amount of deficiency to be borne by E.

(a) ₹ 1,000

(b) ₹ 4,000

(c) ₹ 8,000

(d) ₹ 2,000

Answer

D

10. At the time of admission of a partner, what will be the effect of the following information?

Balance in Workmen Compensation Reserve (WCR) ₹ 40,000. Claim for workmen compensation ₹ 45,000.

(a) ₹ 45,000 Debited to the Partner’s Capital Account

(b) ₹ 40,000 Debited to Revaluation Account

(c) ₹ 5,000 Debited to Revaluation Account

(d) ₹ 5,000 Credited to Revaluation Account

Answer

C

11. In the absence of partnership deed, a partner is entitled to an interest on the amount of additional capital advanced by him to the firm at a rate of

(a) entitled for 6% p.a. on their additional capital, only when there are profits.

(b) entitled for 10% p.a. on their additional capital.

(c) entitled for 12% p.a. on their additional capital.

(d) not entitled for any interest on their additional capitals.

Answer

D

12. Revaluation of assets at the time of reconstitution is necessary because their present value may be different from their

(a) market value

(b) net value

(c) cost of asset

(d) book value

Answer

A

13. If average capital employed in a firm is ₹ 8,00,000, average of actual profits is ₹ 1,80,000 and normal rate of return is10%, then value of goodwill as per capitalisation of average profits is

(a) ₹ 10,00,000

(b) ₹ 18,00,000

(c) ₹ 80,00,000

(d) ₹ 78,20,000

Answer

A

14. In which of the following situation Companies Act, 2013 allows for issue of shares at discount?

(a) Issued to vendors

(b) Issued to public

(c) Issued as sweat equity

(d) None of these

Answer

C

15. As per Section 52 of Companies Act, 2013, securities premium reserve cannot be utilised for

(a) writing-off capital losses.

(b) issue of fully paid bonus shares.

(c) writing-off discount on issue of securities.

(d) writing-off preliminary expenses.

Answer

A

16. Net assets minus capital reserve is

(a) purchase consideration

(b) goodwill

(c) total assets

(d) liquid assets

Answer

A

17. Kalki and Kumud were partners sharing profits and losses in the ratio of 5:3. On 1st April, 2021 they admitted Kaushtubh as a new partner and new ratio was decided as 3:2:1. Goodwill of the firm was valued as ₹ 3,60,000. Kaushtubh couldn’t bring any amount for goodwill. Amount of goodwill share to be credited to Kalki and Kumud Account’s will be

(a) ₹ 37,500 and ₹ 22,500 respectively.

(b) ₹ 30,000 and ₹ 30,000 respectively.

(c) ₹ 36,000 and ₹ 24,000 respectively.

(d) ₹ 45,000 and ₹ 15,000 respectively.

Answer

D

18. Sarvesh, Sriniketan and Srinivas are partners in the ratio of 5:3: 2. If Sriniketan’s share of profit at the end of the year amounted to ₹ 1,50,000, what will be Sarvesh’s share of profit?

(a) ₹ 5,00,000

(b) ₹ 1,50,000

(c) ₹ 3,00,000

(d) ₹ 2,50,000

Answer

D

Section – B

19. Angle and Circle were partners in a firm. Their balance sheet showed Furniture at ₹ 2,00,000; Stock at ₹ 1,40,000; Debtors at ₹ 1,62,000 and Creditors at ₹ 60,000. Square was admitted and new profit sharing ratio was agreed at 2:3:5. Stock was revalued at ₹ 1,00,000, Creditors of ₹ 15,000 are not likely to be claimed, Debtors for ₹ 2,000 have become irrecoverable and Provision for doubtful debts to be provided @ 10%. Angle’s share in loss on revaluation amounted to ₹ 30,000. Revalued value of furniture will be

(a) ₹ 2,17,000

(b) ₹ 1,03,000

(c) ₹ 3,03,000

(d) ₹ 1,83,000

Answer

D

20. Asha and Nisha are partner’s sharing profits in the ratio of 2:1. Kashish was admitted for 1/4 share of which 1/8 was gifted by Asha. The remaining was contributed by Nisha.

Goodwill of the firm is valued at ₹ 40,000. How much amount for goodwill will be credited to Nisha’s Capital account?

(a) ₹ 2,500

(b) ₹ 5,000

(c) ₹ 20,000

(d) ₹ 40,000

Answer

B

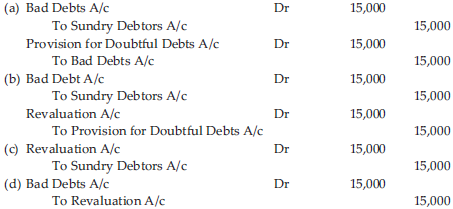

21. At the time of admission of new partner Vasu, old partners Paresh and Prabhav had debtors of ₹ 6,20,000 and a provision for doubtful debts of ₹ 20,000 in their books. As per terms of admission, assets were revalued, and it was found that debtors worth ₹ 15,000 had turned bad and hence should be written-off. Which journal entry reflects the correct accounting treatment of the above situation?

Answer

A

22. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) Transfer to reserves is shown in P and L Appropriation A/c. Reason (R) Reserves are charge against the profits.

In the context of the above statements, which one of the following is correct?

(a) Assertion (A) is correct, but Reason (R) is wrong

(b) Both Assertion (A) and Reason (R) are correct

(c) Assertion (A) is wrong, but Reason (R) is correct

(d) Both Assertion (A) and Reason (R) are wrong

Answer

A

23. Anubhav, Shagun and Pulkit are partners in a firm sharing profits and losses in the ratio of 2:2:1. On 1st April, 2021, they decided to change their profit sharing ratio to 5:3:2. On that date, debit balance of Profit and Loss A/c ₹ 30,000 appeared in the balance sheet and partners decided to pass an adjusting entry for it. Which of the undermentioned options reflect correct treatment for the above treatment?

(a) Shagun’s capital account will be debited by ₹ 3,000 and Anubhav’s capital account credited by ₹ 3,000.

(b) Pulkit’s capital account will be credited by ₹ 3,000 and Shagun’s capital account will be credited by ₹ 3,000.

(c) Shagun’s capital account will be debited by ₹ 30,000 and Anubhav’s capital account will be credited by ₹ 30,000.

(d) Shagun’s capital account will be debited by ₹ 3,000 and Anubhav’s and Pulkit’s capital account will be credited by ₹ 2,000 and ₹ 1,000 respectively.

Answer

A

24. A, B and C are partners, their partnership deed provides for interest on drawings at 8% per annum. B withdrew a fixed amount in the middle of every month and his interest on drawings amounted to ₹ 4,800 at the end of the year. What was the amount of his monthly drawings?

(a) ₹ 10,000

(b) ₹ 5,000

(c) ₹ 1,20,000

(d) ₹ 48,000

Answer

A

25. Abhay and Baldwin are partners sharing profit in the ratio 3:1. On 31st March, 2021, firm’s net profit is ₹ 1,25,000. The partnership deed provided interest on capital to Abhay and Baldwin ₹ 15,000 and ₹ 10,000 respectively and interest on drawings for the year amounted to ₹ 6,000 from Abhay and ₹ 4,000 from Baldwin. Abhay is also entitled to commission @10% on net divisible profits. Calculate profit to be transferred to partner ’s capital accounts.

(a) ₹ 1,00,000

(b) ₹ 1,10,000

(c) ₹ 1,07,000

(d) ₹ 90,000

Answer

A

26. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) Revaluation A/c is prepared at the time of admission of a partner.

Reason (R) It is required to adjust the values of assets and liabilities at the time of admission of a partner, so that the true financial position of the firm is reflected.

In the context of the above two statements, which of the following is correct?

(a) Both Assertion (A) and Reason (R) are correct and Reason (R) is the correct reason of Assertion (A)

(b) Both Assertion (A) and Reason (R) are correct, but Reason (R) is not the correct reason of Assertion (A)

(c) Only Reason (R) is correct

(d) Both Assertion (A) and Reason (R) are wrong

Answer

A

27. Apaar Ltd forfeited 4,000 shares of ₹ 20 each, fully called-up, on which only application money of ₹ 6 has been paid. Out of these 2,000 shares were reissued and ₹ 8,000 has been transferred to capital reserve. Calculate the rate at which these shares were reissued.

(a) ₹ 20 per share

(b) ₹ 18 per share

(c) ₹ 22 per share

(d) ₹ 8 per share

Answer

B

28. Which of the following statement is/are true?

(i) Authorised Capital < Issued Capital

(ii) Authorised Capital ³ Issued Capital

(iii) Subscribed Capital £ Issued Capital

(iv) Subscribed Capital > Issued Capital

(a) Only (i)

(b) Both (i) and (iv)

(c) Both (ii) and (iii)

(d) Only (ii)

Answer

C

29. Mickey, Tom and Jerry were partners in the ratio of 5 : 3 : 2. On 31st March, 2021, their books reflected a net profit of ₹ 2,10,000. As per the terms of the partnership deed they were entitled for interest on capital which amounted to ₹ 80,000, ₹ 60,000 and ₹ 40,000 respectively. Besides this a salary of ₹ 60,000 each was payable to Mickey and Tom.

Calculate the ratio in which the profits would be appropriated.

(a) 1:1:1

(b) 5:3:2

(c) 7:6:2

(d) 4:3:2

Answer

C

30. Mohit had been allotted for 600 shares by a Govinda Ltd on pro rata basis which had issued two shares for every three applied. He had paid application money of ₹ 3 per share and could not pay allotment money of ₹ 5 per share. First and final call of ₹ 2 per share was not yet made by the company. His shares were forfeited. The following entry will be passed

Equity Share Capital A/c Dr ₹ X

To Share Forfeited A/c ₹ Y

To Equity Share Allotment A/c ₹ Z

Here X, Y and Z are

(a) ₹ 6,000; ₹ 2,700; ₹ 3,000 respectively

(b) ₹ 9,000; ₹ 2,700; ₹ 4,500 respectively

(c) ₹ 4,800; ₹ 2,700; ₹ 2,100 respectively

(d) ₹ 7,200; ₹ 2,700; ₹ 4,500 respectively

Answer

C

31. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) In case of shares issued on prorata basis, excess money received at the time of application can be utilised till allotment only.

Reason (R) Company has to pay interest on calls-in-advance @12% p.a. for amount adjusted towards calls (if any).

In the context of the above two state-ments, which of the following is correct?

(a) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A)

(b) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct reason of Assertion (A)

(c) Both Assertion (A) and Reason (R) are false

(d) Assertion (A) is false, but Reason (R) is true

Answer

D

32. Ajay and Vinod are partners in the ratio of 3:2. Their fixed capital were ₹ 3,00,000 and ₹ 4,00,000 respectively.

After the close of accounts for the year it was observed that the interest on capital which was agreed to be provided at 5% p.a. was erroneously provided at 10% p.a. By what amount will Ajay’s account be affected if partners decide to pass an adjustment entry for the same?

(a) Ajay’s Current A/c will be debited by ₹ 15,000.

(b) Ajay’s Current A/c will be credited by ₹ 6,000.

(c) Ajay’s Current A/c will be credited by ₹ 35,000.

(d) Ajay’s Current A/c will be Debited by ₹ 20,000.

Answer

B

33. Vishnu Ltd, forfeited 20 shares of ₹ 10 each, ₹ 8 called-up, on which John had paid application and allotment money of ₹ 5 per share, of these, 15 shares were reissued to Parker as fully paid up for ₹ 6 per share. What is the balance in the Share Forfeiture Account after the relevant amount has been transferred to Capital Reserve Account?

(a) ₹ 0

(b) ₹ 5

(c) ₹ 25

(d) ₹ 100

Answer

C

34. Newfound Ltd took over business of Old Land Ltd and paid for it by issue of 30,000, Equity Shares of ₹ 100 each at a par along with 6% Preference Shares of ₹ 1,00,00,000 at a premium of 5% and a cheque of ₹ 8,00,000. What was the total agreed purchase consideration payable to Old Land Ltd?

(a) ₹ 1,05,00,000

(b) ₹ 1,43,00,000

(c) ₹ 1,40,00,000

(d) ₹ 1,35,00,000

Answer

B

35. A and B are partners in the ratio of 3:2. C is admitted as a partner and he takes 1/4 th of his share from A. B gives 3/16th from his share to C. What is the share of C?

(a) 1/4

(b) 1/16

(c) 1/6

(d) None of these

Answer

A

36. Krishan Ltd has issued capital of ₹ 20,00,000 Equity Shares of ₹ 10 each. Till date ₹ 8 per share have been called-up and the entire amount received except calls of ₹ 4 per share on 800 shares and ₹ 3 per share from another holder who held 500 shares. What will be amount appearing as ‘Subscribed but not fully paid capital’ in the balance sheet of the company?

(a) ₹ 2,00,00,000

(b) ₹ 1,95,99,000

(c) ₹ 1,59,95,300

(d) ₹ 1,99,95,300

Answer

C

Section – C

Bright Star Limited is engaged in manufacture of high-end medical equipment. Considering the prospects of high growth in this segment the company has decided to expand and for this purpose additional investment of ₹ 50,00,00,000 is required. Directors have decided that 20% of this requirement would be financed by raising long-term debts and balance by issue of equity shares.

As per memorandum of association of the company the face value of equity shares is ₹ 100 each. Also, considering the market standing of the company these shares would be issued at a premium of 25%. Directors decided to issue sufficient shares to collect the desired amount (including premium). The prospectus was issued to public, and the issue was oversubscribed by 2,00,000 shares which were issued letters of regret. Answer the below mentioned questions considering that the entire amount was payable on application.

37. What is the total amount collected on application?

(a) ₹ 42,50,00,000

(b) ₹ 40,00,00,000

(c) ₹ 32,00,00,000

(d) None of these

Answer

A

38. How many equity shares were offered for issue by Bright Star Ltd?

(a) 40,00,000 shares

(b) 50,00,000 shares

(c) 35,00,000 shares

(d) 32,00,000 shares

Answer

D

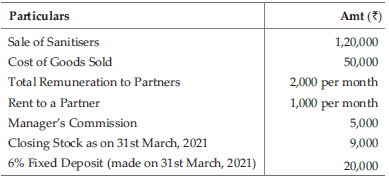

On 1st September, 2020, twenty students of Modern College started their Partnership Firm in the name of ‘‘Be Safe’’ for selling sanitisers on digital mode. Since they were good friends of each other, they were not having any explicit agreement in place. All of them have agreed to invest ₹ 15,000 each as capital. The books were closed on 31stMarch, 2021, on which date the following information was provided by the firm.

39. Calculate the amount of profits to be transferred to Profit and Loss Appropriation Account.

(a) Profit ₹ 58,000

(b) Profit ₹ 44,000

(c) Profit ₹ 59,200

(d) Profit ₹ 58,700

Answer

A

40. On 31st March, 2021, remuneration to partners will be provided to the partners of ‘‘Be Safe’’ but only out of

(a) profits for the accounting year

(b) reserves

(c) accumulated profits

(d) goodwill

Answer

A

41. On 1st December, 2020 one of the partners of the firm introduced additional capital of ₹ 30,000 and also advanced a loan of ₹ 40,000 to the firm. Calculate the amount of interest that partner will receive for the current accounting period.

(a) ₹ 4,200

(b) ₹ 1,400

(c) ₹ 1,575

(d) ₹ 800

Answer

D

Part – II

Section – A

42. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) The focus of calculation of working capital revolves around managing the operating cycle of the business.

Reason (R) It is because the concept of operating cycle is required to ascertain the liquidity of assets and urgency of payments to liabilities.

In the context of the above two statements, which of the following is correct?

(a) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A)

(b) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A)

(c) Both Assertion (A) and Reason (R) are false

(d) Assertion (A) is false, but Reason (R) is true

Answer

B

43. Which of the following are included in traditional classification of ratios?

(i) Liquidity Ratios.

(ii) Statement of Profit and Loss Ratios.

(iii) Balance Sheet Ratios.

(iv) Profitability Ratios.

(v) Composite Ratios.

(vi) Solvency Ratios.

Codes

(a) (ii), (iii) and (v)

(b) (i), (iv) and (vi)

(c) (i), (ii) and (vi)

(d) All (i), (ii), (iii), (iv), (v), (vi)

Answer

A

44. The following groups of ratios primarily measure risk.

(a) Solvency, activity and profitability

(b) Liquidity, efficiency and solvency

(c) Liquidity, activity and profitability

(d) Liquidity, solvency and profitability

Answer

D

45. Which one of the following is correct?

(i) A ratio is an arithmetical relationship of one number to another number.

(ii) Liquid ratio is also known as acid test ratio.

(iii) Ideally-accepted current ratio is 1:1.

(iv) Debt-equity ratio is the relationship between outsider’s funds and shareholder’s funds.

In the context of the above statements, which of the following options is correct?

(a) All (i), (ii), (iii) and (iv) are correct

(b) Only (i), (ii) and (iv) are correct

(c) Only (ii), (iii) and (iv) are correct

(d) Only (ii) and (iv) are correct

Answer

B

46. Which of the following are the tools of Vertical Analysis?

(i) Ratio Analysis.

(ii) Comparative Statements.

(iii) Common Size Statements.

Codes

(a) Only (iii)

(b) Both (i) and (iii)

(c) Both (i) and (ii)

(d) Only (i)

Answer

B

47. Match the items given in column I with the headings/sub-headings (Balance Sheet) as defined in Schedule III of Companies Act, 2013.

Codes

A B C D E

(a) (i) (ii) (iv) (iii) (v)

(b) (iv) (i) (ii) (iii) (v)

(c) (iv) (i) (ii) (ii) (iii)

(d) (v) (iv) (i) (ii) (iii)

Answer

B

48. Which ratio indicates the proportion of assets financed out of shareholder’s funds?

(a) Debt-equity ratio

(b) Fixed assets turnover ratio

(c) Proprietory ratio

(d) Total assets to debt ratio

Answer

C

Section – BSection – B

49. If total sales is ₹ 2,50,000 and credit sales is 25% of cash sales. The amount of credit sales is

(a) ₹ 50,000

(b) ₹ 2,50,000

(c) ₹ 16,000

(d) ₹ 3,00,000

Answer

A

50. What will be the amount of gross profit of a firm if its average inventory is ₹ 80,000, inventory turnover ratio is 6 times, and the selling price is 25% above cost?

(a) ₹ 1,20,000

(b) ₹ 1,60,000

(c) ₹ 2,00,000

(d) None of these

Answer

A

51. Which of the following statements are false?

(i) When all the comparative figures in a balance sheet are stated as percentage of the total, it is termed as horizontal analysis.

(ii) When financial statements of several years are analysed, it is termed as vertical analysis.

(iii) Vertical analysis is also termed as time series analysis.

Codes

(a) Both (i) and (ii)

(b) Both (i) and (iii)

(c) Both (ii) and (iii)

(d) All three (i), (ii), (iii)

Answer

D

52. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) Increasing the value of closing inventory increases profit.

Reason (R) Increasing the value of closing inventory reduces cost of goods sold.

In the context of the above two statements, which of the following is correct?

(a) Both Assertion (A) and Reason (R) are correct and Reason (R) is the correct reason of Assertion (A)

(b) Both Assertion (A) and Reason (R) are correct, but Reason (R) is not the correct reason of Assertion (A)

(c) Only Reason (R) is correct

(d) Both Assertion (A) and Reason (R) are wrong

Answer

A

53. Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R).

Assertion (A) A high operating ratio indicates a favourable position.

Reason (R)Ahigh operating ratio leaves a highmargin tomeet non-operating expenses.

In the context of the above two statements, which of the following is correct?

(a) Both Assertion (A) and Reason (R) are correct and Reason (R) is the correct explanation of Assertion (A)

(b) Both Assertion (A) and Reason (R) are correct, but Reason (R) does not explain Assertion (A)

(c) Both Assertion (A) and Reason (R) are incorrect

(d) Assertion (A) is correct, but Reason (R) is incorrect

Answer

C

54. Current ratio of Adaar Ltd, is 2.5:1. Accountant wants to maintain it at 2:1. Following options are available.

(i) He can repay bills payable (ii) He can purchase goods on credit

(iii) He can take short-term loan

Codes

(a) Only (i) is correct

(b) Only (ii) is correct

(c) Only (i) and (iii) are correct

(d) Only (ii) and (iii) are correct

Answer

D

55. Acompany has an operating cycle of eight months. It has accounts receivables amounting to ₹ 1,00,000 out of which ₹ 60,000 have a maturity period of 11 months. How would this information be presented in the balance sheet?

(a) ₹ 40,000 as current assets and ₹ 60,000 as non-current assets.

(b) ₹ 60,000 as current assets and ₹ 40,000 as non-current assets.

(c) ₹ 1,00,000 as non-current assets.

(d) ₹ 1,00,000 as current assets.

Answer

D